Preliminary Financial Report FY21

One of the City Controller’s primary responsibilities is analyzing and reporting on the City’s financial health. The Preliminary Financial Report, made available each October after the City closes its books, is the first of such report each year. It provides information on how the City spent its money over the past fiscal year, with data and analysis of the City’s revenues and expenditures, reserves and bonded indebtedness.

Last year was unlike any other in the City’s history. Although the fiscal year ended solidly because of spending cuts and the infusion of federal funds, tough choices will almost certainly arise next year’s budget. Scroll below to view the report summary with interactive data visualizations, followed by the full text of the report.

Revenues

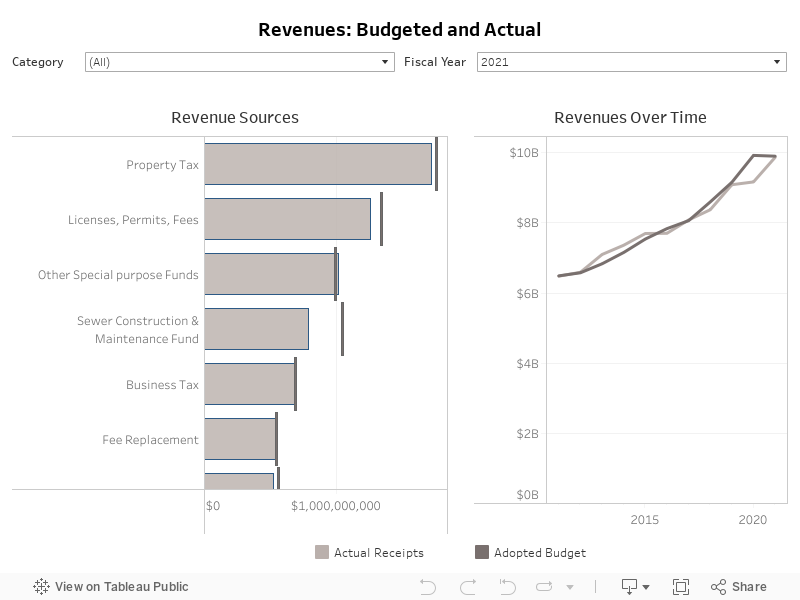

During the 2020-21 fiscal year, total revenues in budgeted funds increased by 0.7%. The COVID-19 pandemic caused revenues to come in 6.8% short of projections. View this interactive data visualization to explore the relative size of the City’s revenue sources and their growth over the past 10 years.

Expenditures

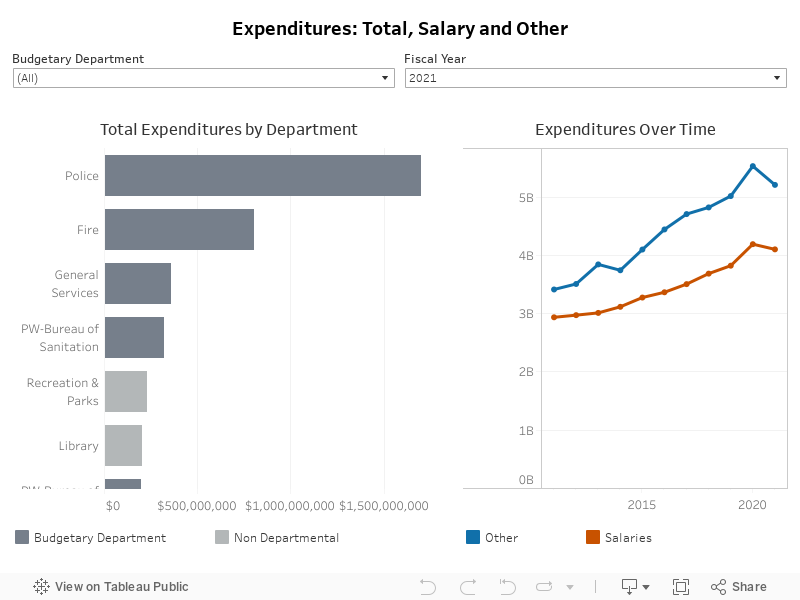

Total budgeted expenditures shrank at a rate of 1.7%, due in large part to a hiring freeze, deferral of employee salary increases and deferral of capital improvement projects. This interactive data visualization compares the expenditures of the City’s different departments, as well as non-departmental expenditures, over the past 10 years.

Reserves

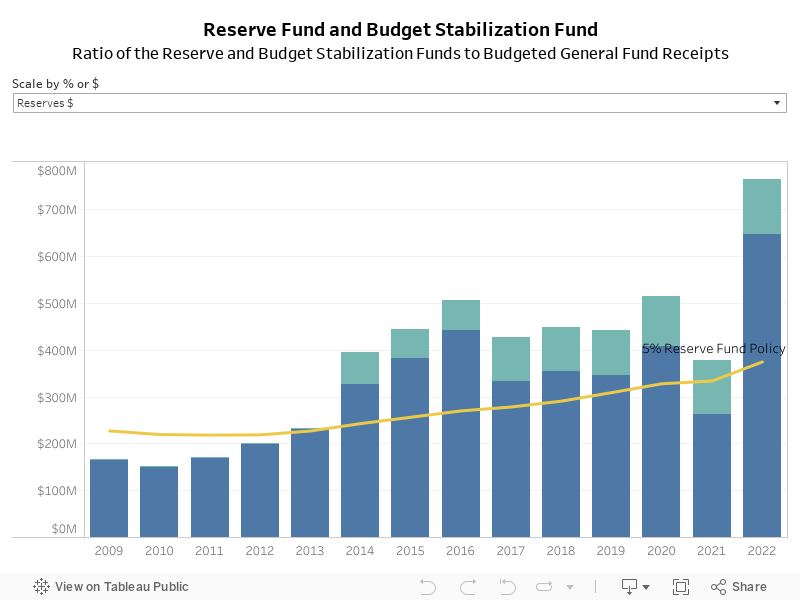

The Reserve Fund is established to ensure that funds are available for unanticipated expenditures and revenue shortfalls in the General Fund. The City’s Reserve Fund Policy sets a goal for the Reserve Fund to be at least 5% of the General Fund budget every year. On July 1, 2021, the Reserve Fund had a balance of $647 million, 8.62% of the General Fund budget and well above the 5% Reserve Fund Policy goal.

The Budget Stabilization Fund (BSF) was added to the City Charter in 2011. The purpose of the BSF is to set aside funds when the City exceeds revenue projections to help smooth out years when revenue is stagnant or in decline. In fiscal year 2021, the BSF grew slightly to $118.2 million and is now 1.6% of General Fund revenues. Click the chart below to view the performance of the Reserve Fund and Budget Stabilization Fund, both in dollar terms and as a percentage of budgeted General Fund revenues.

Debt

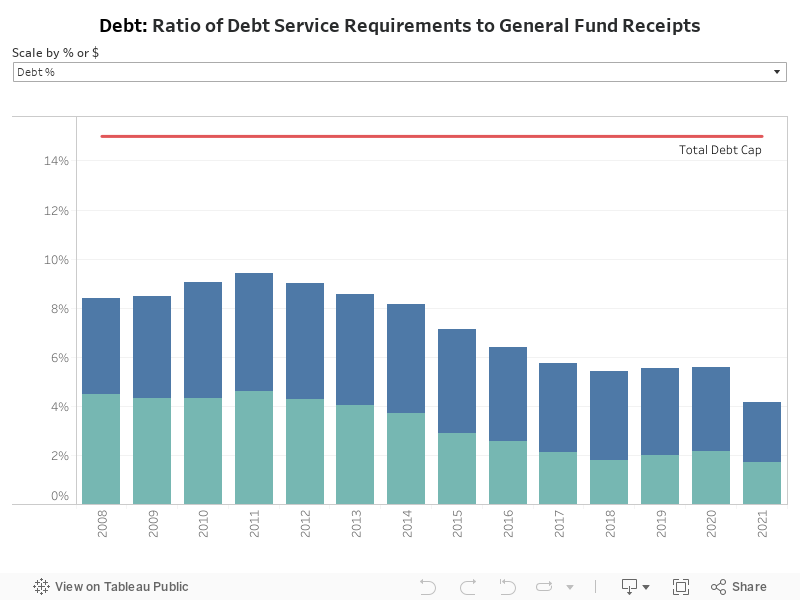

The City’s debt management policy establishes guidelines for the structure and management of the City’s debt obligations. These guidelines include a non-voter-approved debt service cap of 6% and a total debt service cap of 15% as a percent of General Fund revenues. The City’s debt service obligations decreased to 4.9% last fiscal year.

Recommendations

The City’s immediate fiscal situation is solid, but to address the challenges of the future, the Controller makes the following recommendations in the Preliminary Financial Report:

Strengthen the City’s revenues and control ongoing costs.

While some revenues have remained strong through the pandemic, others have decreased significantly. It is critical to the City’s recovery that revenue generation and collection be restored. At the same time, the City must limit the growth of ongoing expenditures so that it does not commit to unsustainable levels of future spending.

Build on successful new programs and consider ending those that are not delivering results.

The 2021-22 budget provides significant funding to begin pilot projects and new programs, many focused on alleviating homelessness and increasing local equity. The City should analyze these efforts critically and commit to ongoing funding only for those programs that demonstrate measurable success.

Maintain the City’s strong Reserve Fund.

After a decade of building up the Reserve Fund, the City used almost $200 million to offset a General Fund shortfall at the end of Fiscal Year 2019-20. Now, with the City’s largest ever Reserve Fund balance, there could be a temptation to treat it as a source of funds for new programs. However, the City should guard these reserved and only use them to fund the most critically important one-time programs or this important tool will not be available the next time Los Angeles needs it.

Utilize the City’s capital program and debt capacity to meet community needs and drive equity.

As part of the effort to reduce expenditures during the first half of Fiscal Year 2020-21, the City cut funding from a large number of capital projects. The capital program will likely be rebuilt in the coming months, providing a perfect opportunity to leverage capital needs and build equity in the City’s under-resourced and historically disadvantaged neighborhoods.

October 21, 2021

Honorable Eric Garcetti, Mayor

Honorable Members of the Los Angeles City Council

Re: Preliminary Financial Report for Fiscal Year 2020-21

The Controller’s Office submits the Preliminary Financial Report (PFR) each fall to review the City of Los Angeles’ financial operations for the prior fiscal year. Our report is the City’s first look back at municipal finances after the close of the fiscal year, providing an overview and analysis of revenues and expenditures, reserves and bonded indebtedness. In early 2022, my office will follow up by issuing the Annual Financial Report for 2020-21, which is prepared in accordance with Generally Accepted Accounting Principles and audited by an independent firm of certified public accountants.

Accompanying the PFR are online interactive visualizations with 10 years of data, which can be found at lacontroller.org/pfr2021. Information on special fund balances and uses, Reserve Fund starting balances over the years, and budget appropriations, adjustments, expenditures and revenues, are also on my website.

The report is prepared to help City leaders understand and assess the state of the City’s finances — an especially important task given that we are still emerging from the COVID-19 pandemic. Despite the unique nature of the economic situation, assessing the impact of the pandemic on revenues and expenditures, reserves and outstanding debt — all of which are discussed in the report — along with the assistance provided by the federal government, is critical to navigating the current fiscal year and those ahead.

Challenging year until help arrived

The first eight months of the previous fiscal year were months of austerity. Hiring freezes, wage cuts, cancelled capital projects and other money-saving measures were implemented to compensate for a projected $600 million budget shortfall. The last four months of the year brought a reversal of fortunes as help arrived. COVID-19 vaccines became widely available, allowing for a partial economic reopening, and the federal government passed the American Rescue Plan Act of 2021 (ARPA), which included $1.28 billion in direct funding to the City, half of which was received in May 2021.

Other facts about the 2020-21 fiscal year highlighted in the PFR are the following:

- Total revenues in budgeted funds were $9.23 billion last year, a 0.7 percent increase over the previous year. This figure does not include ARPA assistance, which helped the City end the year in a cash surplus.

- Total expenditures were $8.8 billion, 1.7 percent lower than the year prior, largely because of the City’s hiring freeze and employee sacrifices.

- The pandemic underscored how essential reserves are to the City and the need to build them when possible. While they were depleted somewhat during fiscal year 2020-21, the adjusted Reserve Fund balance in July 2021 was $647 million or 8.62 percent of General Fund receipts anticipated in the current budget — higher than it has ever been.

Difficult decisions loom

Although the PFR reviews last fiscal year’s numbers, which ended solidly thanks to the infusion of ARPA funds, next year could bring different budgeting challenges. One notable issue is the use of one-time ARPA funding, which allowed the creation of most of the new programming in the 2021-22 budget. This funding will not be available to continue these programs in 2022-23, as all of it is spoken for in the current budget — a reality that could force some tough decisions about the continuation of these programs in the next budget. In addition, the current budget includes almost $300 million in programs funded by prior year appropriations, including $70 million reallocated from the Police Department in July 2020. The City needs to thoroughly and honestly assess the performance of these programs over the course of the year to determine which are successful and which fall short of their goals.

Another worry is increased expenses in the form of pay and benefits for City employees, many of whom will receive raises soon and see new labor contracts negotiated thereafter. Greater costs could hinder the City’s ability to maintain services, especially if the economy does not rebound as projected. To proactively address these issues, my office recommends that the City focus on increasing revenues where possible and limit spending on novel programs and department requests.

Use capital program and debt financing to promote equity

The City’s debt service requirements decreased from 5.6 percent to 4.9 percent of General Fund revenues last fiscal year, remaining considerably below the 15 percent policy limit. The significant level of debt capacity presents the City with an opportunity to explore additional debt financing opportunities, which could help create jobs and improve neighborhoods through infrastructure projects. These efforts should benefit areas of Los Angeles that were disproportionately impacted by the pandemic and in historically disadvantaged communities to achieve greater regional equity.

My staff and I appreciate the cooperation shown by City departments as we prepared the PFR. Should you have questions or need more information, please contact my Director of Financial Analysis and Reporting, Matthew Crawford: (213) 978-7203 or matthew.crawford@lacity.org.

Respectfully submitted,

RON GALPERIN

L.A. Controller

cc: Sharon Tso, Chief Legislative Analyst

Matt Szabo, City Administrative Officer

At the close of each fiscal year, the Office of the Controller reports on the finances of the City for the year that recently closed. This Preliminary Financial Report is the first part of that reporting and provides cash basis information on revenues, expenditures, reserves, and bonded indebtedness, including comparisons to the prior year and to the Budget.

The second part of this reporting requirement is the Annual Financial Report (AFR), the City’s official, audited financial statement, which will be released later this fiscal year. Together, these two documents educate and inform both City decision-makers and the public on the City’s financial position.

A Year of Uncertainty

Fiscal year 2020-21 began in a state of widespread uncertainty. The nation was three months into the COVID-19 pandemic with stay-at-home emergency orders in place. The impact the pandemic would have on the City’s economy was unknown, and the potential for assistance from the federal government was unclear. Due to this uncertainty, the City Council did not revise the Mayor’s Proposed Budget as it usually does, but left it instead to become “the official budget” in accordance with the City Charter, acknowledging that revisions would be necessary throughout the year. By the end of June 2020, it was clear that the financial and social landscape had already changed, and the Council passed significant budget amendments on July 1.

For the first eight months of the Fiscal Year, the City operated in an environment of austerity. Hiring freezes, mandatory budget reductions, amended labor contracts, deferral or cancellation of capital projects, and a Separation Incentive Plan were all implemented in order to mitigate what was at one point projected to be a revenue shortfall of more than $600 million.

The final third of the Fiscal Year saw a reversal of fortunes. COVID-19 vaccines became widely available, allowing for a partial economic reopening. The federal government passed the American Rescue Plan Act of 2021 (ARPA), which included direct funding to the City of almost $1.3 billion, half of which was received in May 2021. Other grants and funding streams from the federal and state governments were also approved bringing much-needed funding for COVID-19 and homelessness response efforts. Fortunately, an uneven economic recovery resulted in General Fund revenues performing better than feared, finishing the year only $317 million below budget.

Combining improved revenues with savings from nine months of hiring freezes and budget cuts, the General Fund ended the year with an unexpectedly large surplus to transfer to the Reserve Fund, which resulted in Fiscal Year 2021-22 starting with a record-high balance of $640 million, $385 million more than twelve months earlier.

The Fiscal Year 2021-22 Budget was adopted with a framework of economic and social recovery, and the second tranche of the ARPA funds and other funding sources were programmed to finance more than $900 million in homelessness response and equity programs. The Budget projects a strong rebound, with 7.7 percent growth in General Fund revenue, not including the ARPA funding. While it is still too early to make accurate projections, the first three months of this Fiscal Year have shown signs of growth.

However, the future will bring significant challenges. Most of the new programming contained in the Fiscal Year 2021-22 Budget is backed by one-time funding which means these new programs will not continue in 2022-23 unless additional funding is identified. In addition, many City employees are due to receive a deferred pay increase at the end of the current Fiscal Year (June 30, 2022), after which most of the City’s Memoranda of Understanding (MOUs) expire. The collective bargaining process that will follow will likely lead to additional long-term obligatory costs, especially as predictions of cost inflation begin to impact decision-making. There are also approximately $300 million in programs in the current year that are funded from prior year appropriations, including almost $70 million in funding that was reallocated from the Police Department in July 2020.

The combination of the cessation of one-time monies, new programs and priorities, and labor negotiations means that the Fiscal Year 2022-23 budget process will inevitably require difficult choices and trade-offs. A renewed Reserve Fund may provide some limited ability to defer these decisions or fund individual projects, but doing so would substantially weaken the City’s ability to weather future economic crises without another round of destabilizing cuts.

Recommendations

-

Strengthen the City’s revenues and control ongoing costs.

While some revenues have remained strong through the current crisis, others have decreased significantly. It is critical to the City’s recovery that revenue generation and collection be restored. At the same time, we must limit growth in the City’s ongoing costs so that we do not commit to unsustainable levels of future spending.

-

Build on successful new programs and consider ending those that are not delivering results.

The Fiscal Year 2021-22 Budget provides significant funding to begin pilot projects and new programs. The City should analyze these efforts critically and commit to ongoing funding only for those programs which demonstrate success.

-

Maintain the City’s strong Reserve Fund.

After a decade of building up the Reserve Fund, the City used almost $200 million to offset a General Fund shortfall at the end of Fiscal Year 2019-20. Now, with the largest Reserve Fund the City has ever had, there will naturally be a temptation to treat it as a source of funds for new programs. However, these reserves should be guarded and only used to fund the most critically important, one-time programs, or this important tool will not be available the next time it is needed.

-

Utilize the City’s capital program and debt capacity to meet critical needs and drive equity.

As part of the effort to reduce expenditures during the first half of Fiscal Year 2020-21, funding was cut from a large number of capital projects. The next budget year will likely see a rebuilding of the City’s capital program, providing a perfect opportunity to leverage capital needs and building equity in the City’s under-resourced and disadvantaged neighborhoods. The City should consider capital projects as another method of reorienting the City’s built environment to benefit historically disadvantaged neighborhoods and people.

Section Summary

The Preliminary Financial Report is organized in four distinct sections:

- Revenues and Expenditures: A discussion of the fiscal year that just ended, including trend analysis, notable changes from prior years, and financial performance relative to the Budget;

- Reserve Fund: A discussion of the current condition of the City’s Reserve Fund, and analysis of the various factors influencing that figure;

- Budget Stabilization Fund: A discussion of the Fund policy and how actual figures compare to the policy; and

- Bonded Indebtedness: A statement of the City’s total bonded indebtedness and debt service requirements; as well as comparisons to City policies and legal limitations.

Revenues and Expenditures

Total Budgeted Revenue was 6.8 percent below the Budget, growing by 0.7 percent over Fiscal Year 2019-20, and 1.6 percent over Fiscal Year 2018-19. General Fund revenue fell by 0.1 percent compared to last year, and was 4.8 percent below the Budget. Significant shortfalls in Transient Occupancy Tax, Sales Tax, Parking Users’ Tax, Departmental Receipts, the Special Parking Revenue Fund transfer, and Parking Fines were partially offset by healthy growth in Property Tax, strong growth in Documentary Transfer Tax, and one-time revenue from federal grants. Revenue in budgeted special funds increased by 2.4 percent over the prior year; however, it was 11.0 percent under the budget due to shortfalls in building permit revenues, State Proposition A revenues, and a delay in Sewer Construction and Maintenance Fund bond issuance. Receipts from the American Rescue Plan Act of 2021 (ARPA) are not included in Budgeted Revenue because the funds were not included in the 2020-21 Budget and the receipts were transferred to the General Fund as cash and not appropriated for spending.

Both expenditures and encumbrances declined, 1.7 and 33.7 percent respectively, from June 30, 2020 to June 30, 2021. While all of the categories of spending dropped, the Capital Improvement Expenditure Program contracted the most, followed by Liability Claims, and Proposition A Local Transit Assistance.

Reserve Fund

The Reserve Fund served its purpose in Fiscal Year 2019-20, when it absorbed the $195.5 million General Fund revenue shortfall. The City also front-funded pandemic related costs using reserves. As a result, the Reserve Fund Balance started Fiscal Year 2020-21 at just 3.9 percent of the General Fund Budget, below the 5 percent policy goal. However, due to the combination of ARPA funds, fourth quarter revenue growth, and reduced General Fund expenditures, the Reserve Fund began Fiscal Year 2021-22 at 8.62 percent of the General Fund Budget.

Budget Stabilization Fund

The Budget Stabilization Fund (BSF) is the City’s mechanism for accumulating excess tax revenues in growth years in order to mitigate shortfalls in lean years. During the year, the BSF was proposed to be used as part of the budget balancing solution. However, as it turned out, such action was unnecessary, and the June 30, 2021 balance in the Fund was $118.2 million.

Bonded Indebtedness

Bonded indebtedness and the City’s debt service obligations decreased due to the defeasance and advance refunding of MICLA Revenue Bonds Series 2014 and 2019 and the lack of any large new issuance of General Obligation Bonds. Debt service payments decreased as well, from 5.6 percent to 4.9 percent of General Fund revenue, and are well under the City’s 15 percent policy ceiling.

Total revenues in budgeted funds for 2020-21 were $9.23 billion, an increase of 0.7 percent compared to 2019-20, and increase of 1.6 percent over 2018-19. The revenues do not include the ARPA funding of $639.5 million received in May that was transferred to the General Fund.

Total expenditures (excluding encumbrances) from budgeted funds decreased by 1.7 percent to $8.8 billion, which includes $516.3 million payments of prior year’s encumbrances. In addition to the expenditures, the City had $516.4 million encumbered as of June 30, 2021.

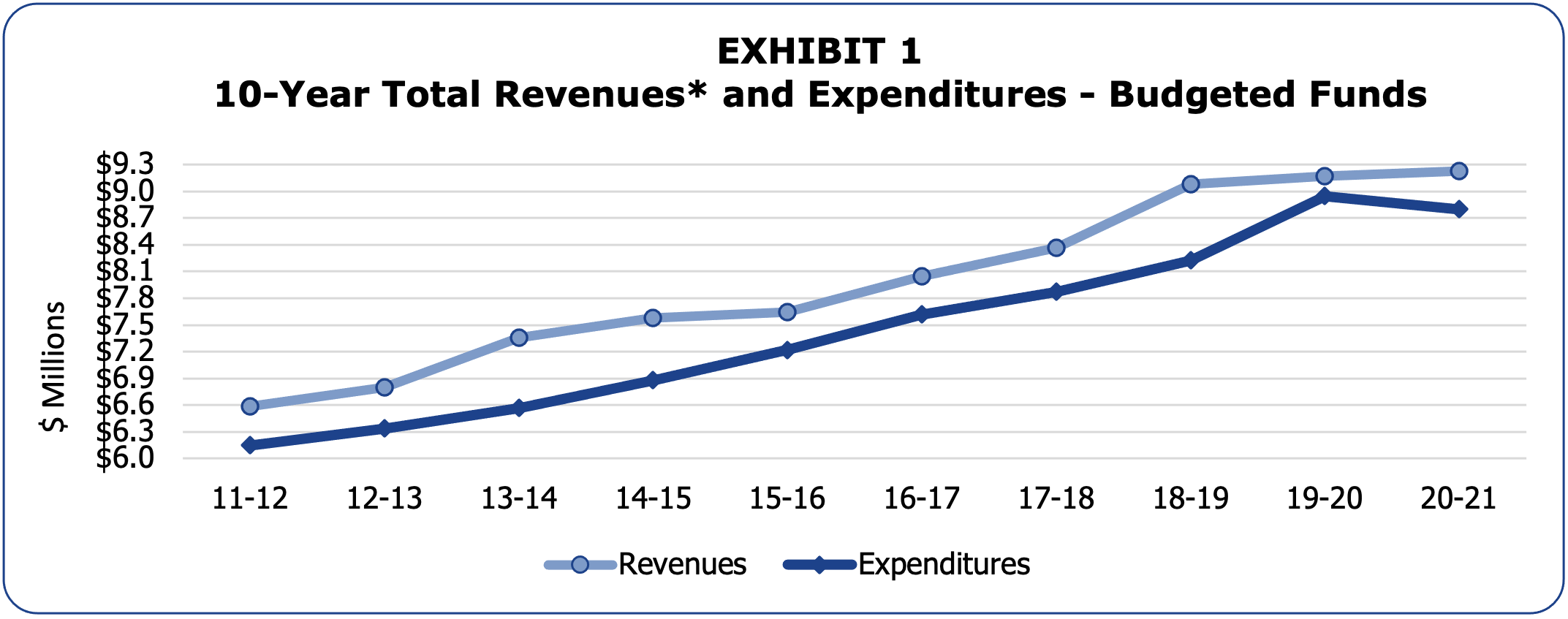

Exhibit 1 shows the ten-year history of total revenues and expenditures.

*Excluding transfers from reserves

Since 2011-12, revenues have grown by 40.2 percent (average annual growth of 3.9 percent), while expenditures have grown by 43.2 percent (average annual growth of 4.1 percent). As seen in Exhibit 1, revenues have consistently exceeded expenditures. Most of this excess has been in the City’s many budgeted special funds. The surplus in the General Fund has been a much smaller portion of the total, but still has allowed the City to grow the Reserve and Budget Stabilization Funds.

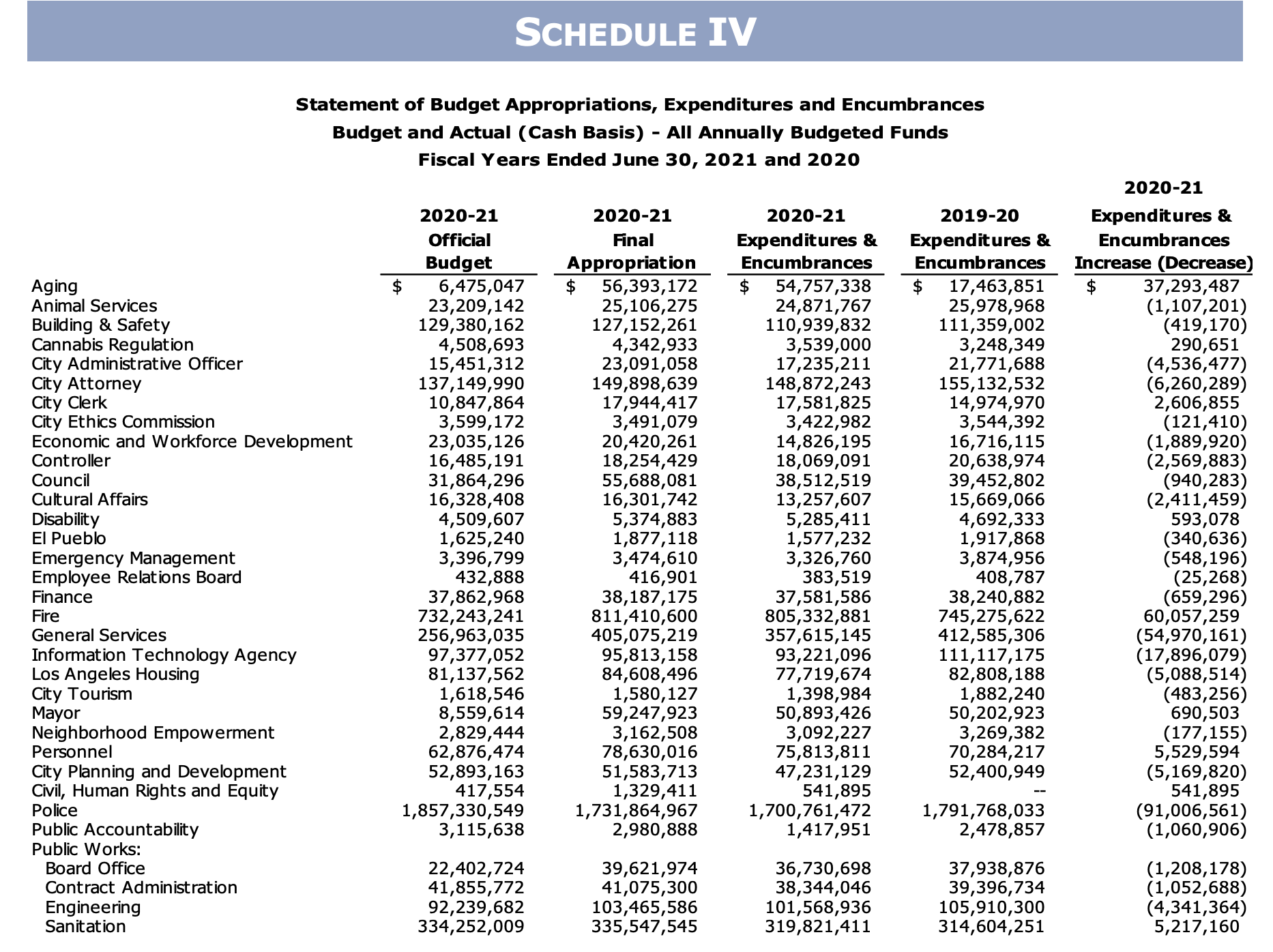

The 2020-21 Budget totaled $9.90 billion (excluding $628.4 million in available balances), of which $6.69 billion was in the General Fund and $3.21 billion was in Special Funds. Actual receipts for the year (again excluding available balances) were $9.23 billion, 6.8 percent less than budgeted, while total expenditures (including encumbrances) were $9.32 billion, 11.5 percent less than budgeted. Detail of budgeted and actual receipts and expenditures is presented in Schedules III and IV.

General Fund Revenues

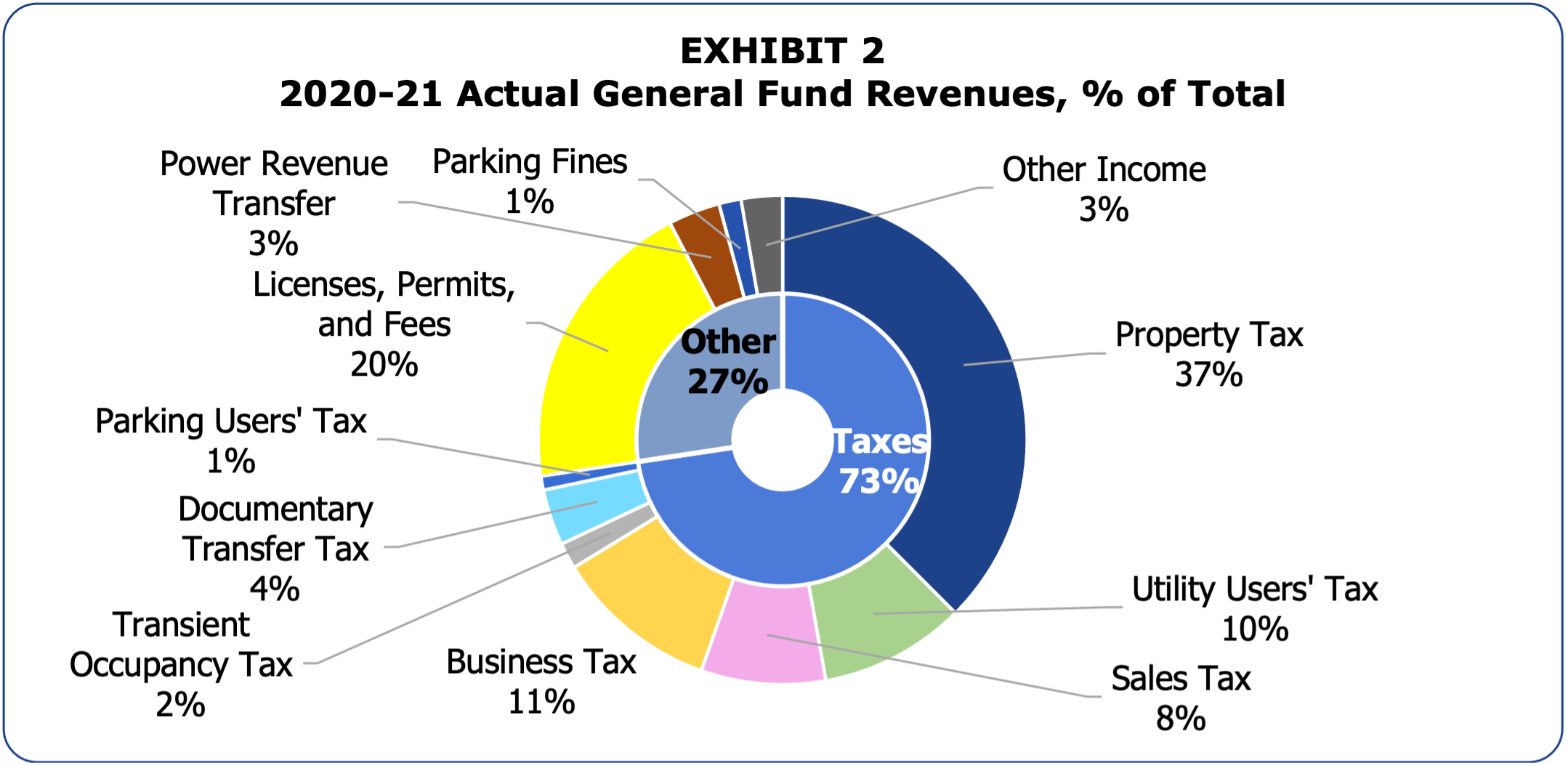

The General Fund is the primary operating fund of the City. It is used to account for all financial resources except those legally required to be accounted for in other funds. General Fund revenues are derived from such sources as taxes, licenses, permits, fees, fines, intergovernmental revenues, charges for services, special assessments, and interest income. Exhibit 2 presents 2020-21 actual General Fund revenues by percentage.

2020-21 General Fund receipts totaled $6.37 billion, $317.4 million (4.8 percent) less than the Budget, $4.25 million (0.1 percent) less than 2019-20, and $138.9 million (2.2 percent) more than 2018-19. Over the past five years, General Fund revenue averaged 3.9 percent growth, slightly exceeding the Budget twice and coming up a little short three times. In Fiscal Year 2020-21, General Fund revenue decreased from the prior year, the first time this occurred in more than a decade. Exhibit 3 presents a comparison between adopted and actual General Fund receipts by fiscal year.

*Excluding transfers from reserves

General Fund revenues that outperformed the Budget in 2020-21 included Business Tax ($5.8 million or 0.9 percent over budget), Documentary Transfer Tax ($20.1 million or 9.3 percent), Franchise Income ($3.1 million or 3.8 percent), Gas User’s Tax ($6.4 million or 9.6 percent), and Grant Receipts ($31.2 million or 248.9 percent).

Property Tax receipts were $129.0 million (6.1 percent) higher than 2019-20 receipts, but lower than the budget by $35.7 million or 1.6 percent. Ex-CRA Property Tax Increment revenue was $32.1 million over the budget and $44.0 million more than the prior year.

The Budget assumed 4.5 percent growth for Business Tax receipts, and actual receipts were 5.6 percent or $36.5 million higher than last year, and 0.9 percent or $5.8 million over the Budget. Recreational cannabis Business Tax generated $136.8 million in revenues, and its share in the total Business Tax grew from 11.9 percent to 19.8 percent. Actual receipts exceeded the Budget by $37.5 million (37.7 percent), and exceeded last year’s total by $58.5 million (74.7 percent). Meanwhile non-cannabis Business Tax actual receipts of $555.6 million were 5.4 percent or $31.6 million lower than the Budget, and 3.8 percent or $22.0 million lower than last year.

Sales Tax Receipts were $31.6 million or 5.7 percent lower than last year, and $32.4 million or 5.8 percent lower than the Budget. Along with pandemic-related closures, the Tax Deferment Program implemented by the State affected the collected revenues. Due to lack of detailed data, it is virtually impossible to differentiate these two impacts, so we do not know how much of the reduced receipts will be recovered in future periods.

Franchise Income ended higher than Budget by $3.1 million, mainly due to Natural Gas Franchise income that exceeded the Budget by $2.4 million.

Utility Users’ Tax was 0.1 percent below the Budget, and 3.6 percent lower than last year’s actual receipts. While Gas Users Tax exceeded the Budget by $6.4 million, Electrical Users and Telephone Users Taxes were a combined $5.7 million (1.0 percent) under the Budget.

Licenses, Permits, Fees and Fines ended $77.8 million or 5.8 percent lower than the Budget, but higher than last year ($59.2 million or 4.9 percent). The picture would have been significantly worse without the $125 million reimbursement of City Expenditures from COVID-19 Federal Relief Fund. Departmental receipts (relating mainly to licenses, permits, and various service fees collected by departments) were $11.9 million below the budgeted amounts. Other components of Licenses, Permits, Fees and Fines were short as well (Emergency Ambulance Services $21.0 million, Services to the Los Angeles County Metropolitan Transportation Authority (LACMTA) $27.9 million, and Services to Proprietary Departments 26.9 million). The shortfall in reimbursements from special funds, excluding the COVID-19 Federal Relief Fund transfer, was $115.1 million.

As a result of the March 22, 2020, Federal Major Disaster Declaration related to the COVID-19 pandemic, the Federal Emergency Management Agency (FEMA) Public Assistance program will reimburse state and local governments for pandemic-related emergency protective measures. The City has applied for, and FEMA has approved, this assistance for the City. As a result, the City received $30.7 million in Fiscal Year 2020-21 and will receive additional reimbursements in future years.

Transient Occupancy Tax (TOT, commonly known as Hotel Tax) receipts experienced the most conspicuous decline, as travel and hospitality virtually stopped. TOT was $134.4 million or 54.9 percent below budget and $143.1 million or 56.5 percent less than last year. Receipts near the end of Fiscal Year 2020-21 and the beginning of the current fiscal year have shown some growth, but still far below pre-COVID levels.

Exhibit 4 shows cumulative Transient Occupancy Tax monthly receipts for FY 2019, FY 2020 and FY 2021.

The pandemic’s impact on the lodging industry will likely continue to evolve, rather than disappear. The level of vaccination and consumer confidence, both domestically and internationally, will determine how quickly the industry will recover and experience to a meaningful acceleration in demand.

Documentary Transfer Tax receipts were $20.1 million or 9.3 percent above the Budget and $30.4 million or 14.8 percent above last year. The pandemic briefly stalled the market at the end of Fiscal Year 2019-20, but home prices continued to rise and sales remained strong, leading to a record high for receipts in this category.

The Power Revenue Transfer was $5.7 million (2.6 percent) less than budget. It has been declining slowly since 2016, with a 3.9 percent average decrease over the last five years.

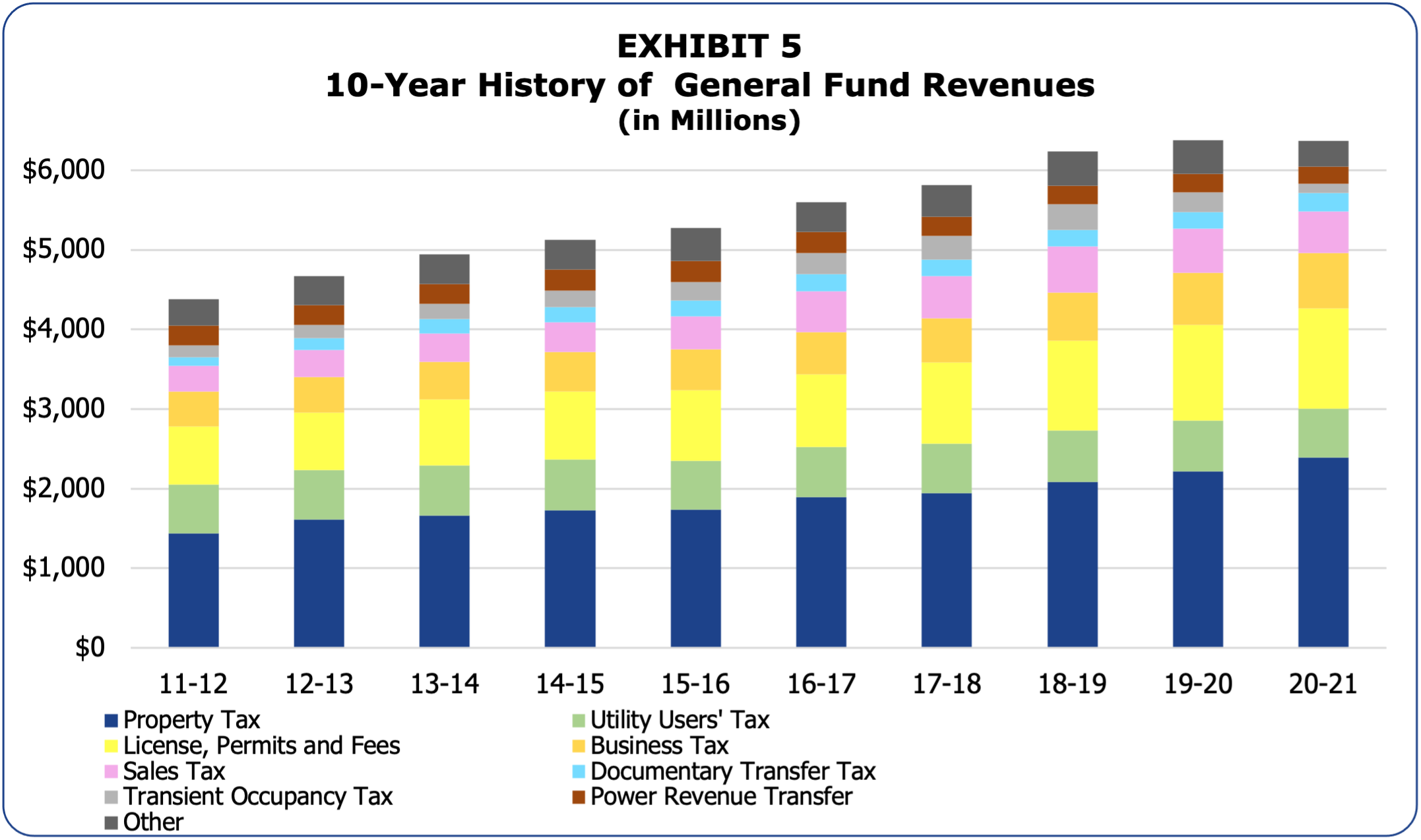

Exhibit 5 displays a 10-year history of General Fund receipts, excluding transfers from the Reserve Fund.

Appropriations, Expenditures & Encumbrances

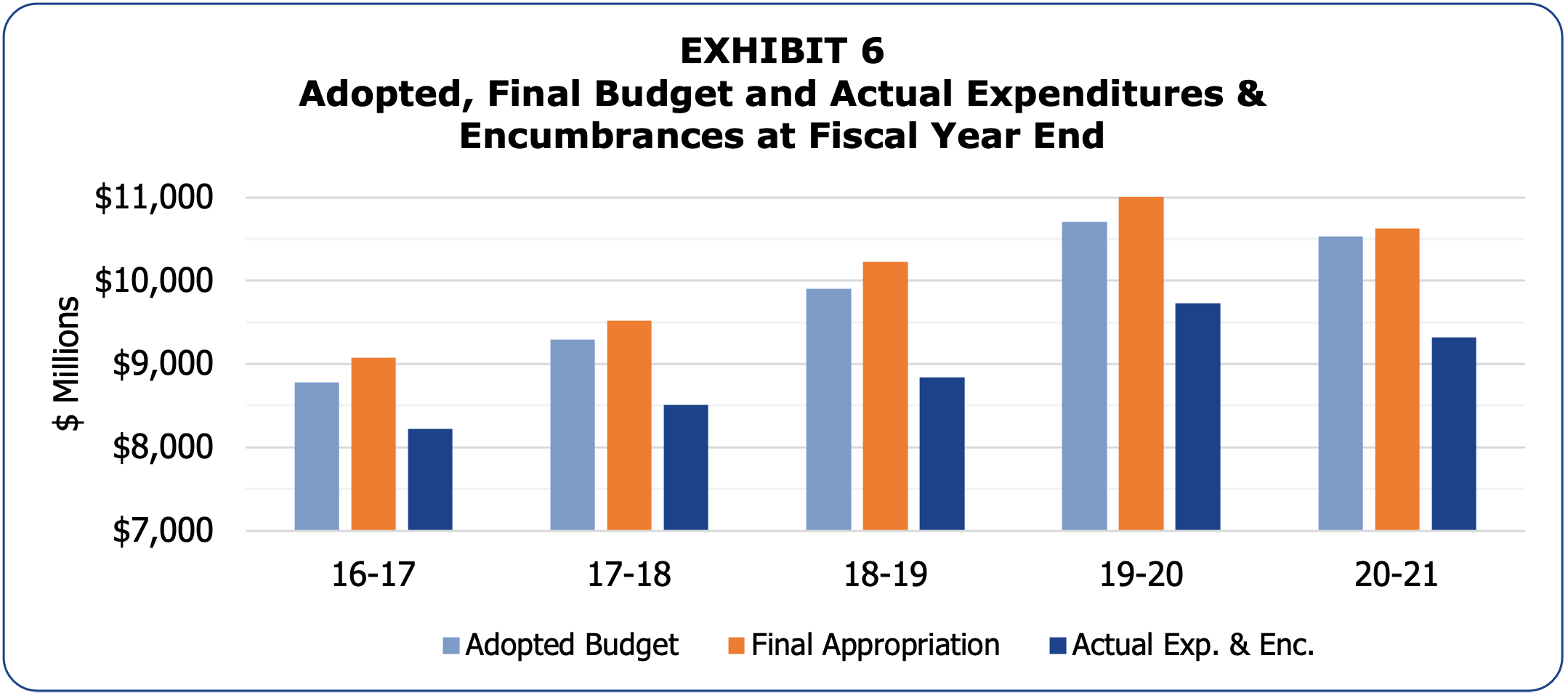

Total expenditures, including encumbrances, were $9.32 billion. This was $410.9 million or 4.2 percent lower than 2019-20, and $1.21 billion or 11.5 percent lower than the Budget.

Exhibit 6 presents a comparison between the Budget, the final appropriation (which includes interim appropriations made during the year), and actual expenditures and encumbrances by fiscal year.

For the last five years total actual Expenditures and Encumbrances have grown by an average of 3.7 percent. For the same period, Salaries (excluding Library and Recreations and Parks) increased by 4.2 percent, and Services, Supplies, Equipment and Others by 5.6 percent. Salaries are made up of Sworn and Civilian Salaries, which increased by 2.7 percent and 4.5 percent respectively.

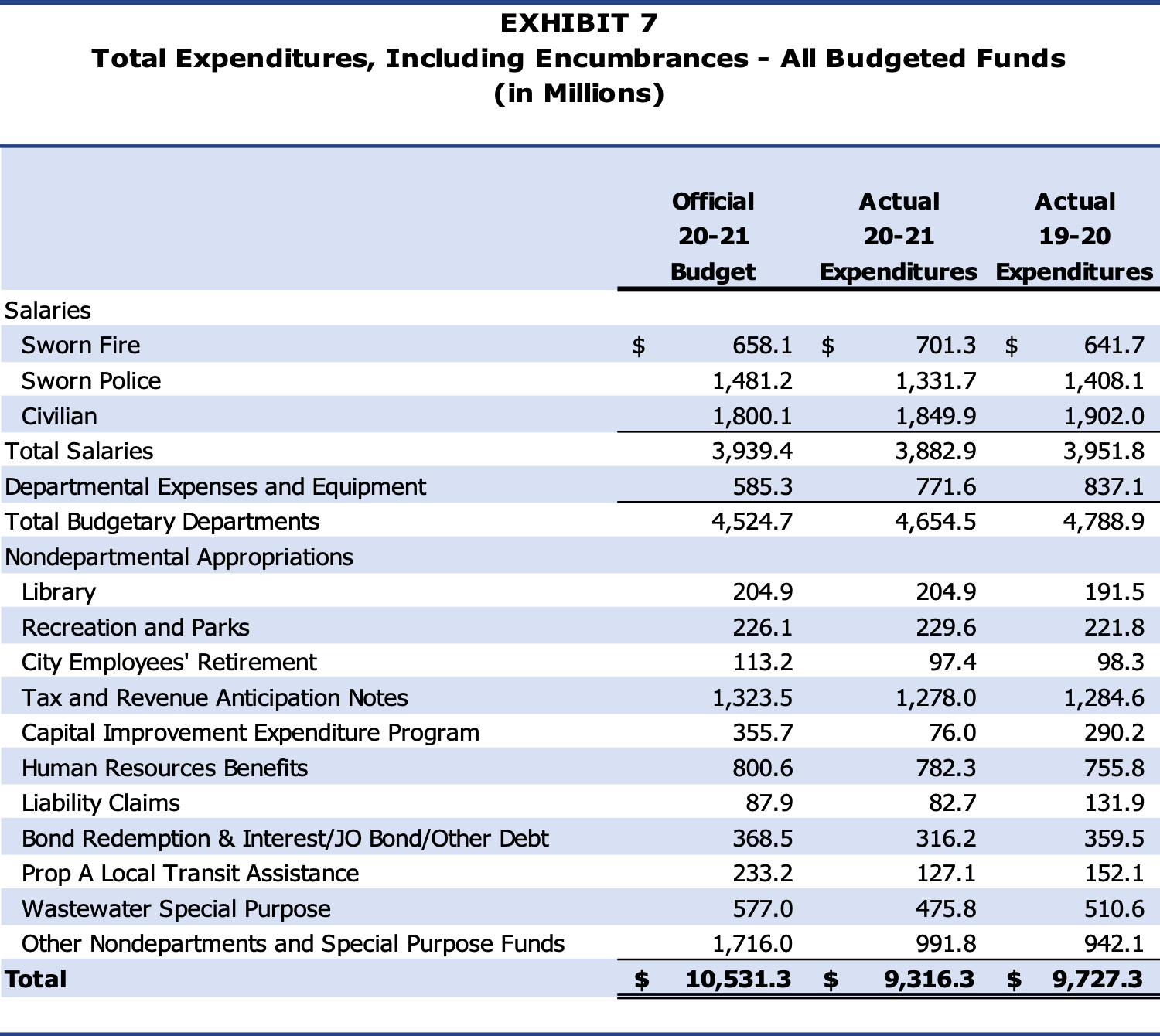

Exhibit 7 breaks out summarized categories of budgetary and actual expenditures and encumbrances for 2019-20 and 2020-21. Detailed information by department can be found in Schedule IV.

Note: Appropriations to Library and Recreation and Parks include both salaries and expense accounts.

Salaries decreased by $68.9 million or 1.7 percent compared to last year mainly due to reduced civilian workforce, labor agreements with most employee organizations to defer compensation adjustments that were set to take effect on 2020-21 and 2021-22 and unpaid days for all civilian employees.

Total contributions to Library and Recreation and Parks, which increased by a $13.4 million or 7.0 percent and $7.8 million or 3.5 percent respectively, are made pursuant to Charter requirements and are tied to growth in the City’s total assessed valuation.

Capital Improvement Expenditure Program (CIEP) expenditures were 78.6 percent or $279.7 million lower than budget, and $214.2 million lower than the prior year. The largest decrease was in Clean Water Projects, $253.9 million compared to Budget, and $178.3 million compared to prior year actual.

Human Resources Benefits expenses were $18.3 million or 2.3 percent below the Budget, but higher by $26.5 million or 3.5 percent compared to last year. The increase was primarily due to increases in health care subsidies for employees, by $21.0 million or 4.1 percent, and Unemployment Insurance costs, which increased by $6.2 million.

Exhibit 8 breaks out expenditures and encumbrances by Governmental Activity.

Almost a third of total expenditures were spent on Protection of Persons and Property. Even as priorities have shifted and the economy has expanded, this percentage has remained remarkably stable.

Also of note were the contributions to the City’s pension systems, which totaled $1.43 billion, 15.3 percent of total spending. This is up slightly from the prior year. To the extent that the City is able to hold salary expenditures under long-term averages, the increase will be mitigated, but this issue should be monitored carefully.

The City ended the Fiscal Year with a total of $516.4 million in encumbrances: $356.8 million in the General Fund and $159.5 million in special funds, $110.9 million was encumbered for salaries to be paid in July 2021, with the balance encumbered in expense, equipment, and special fund project accounts.

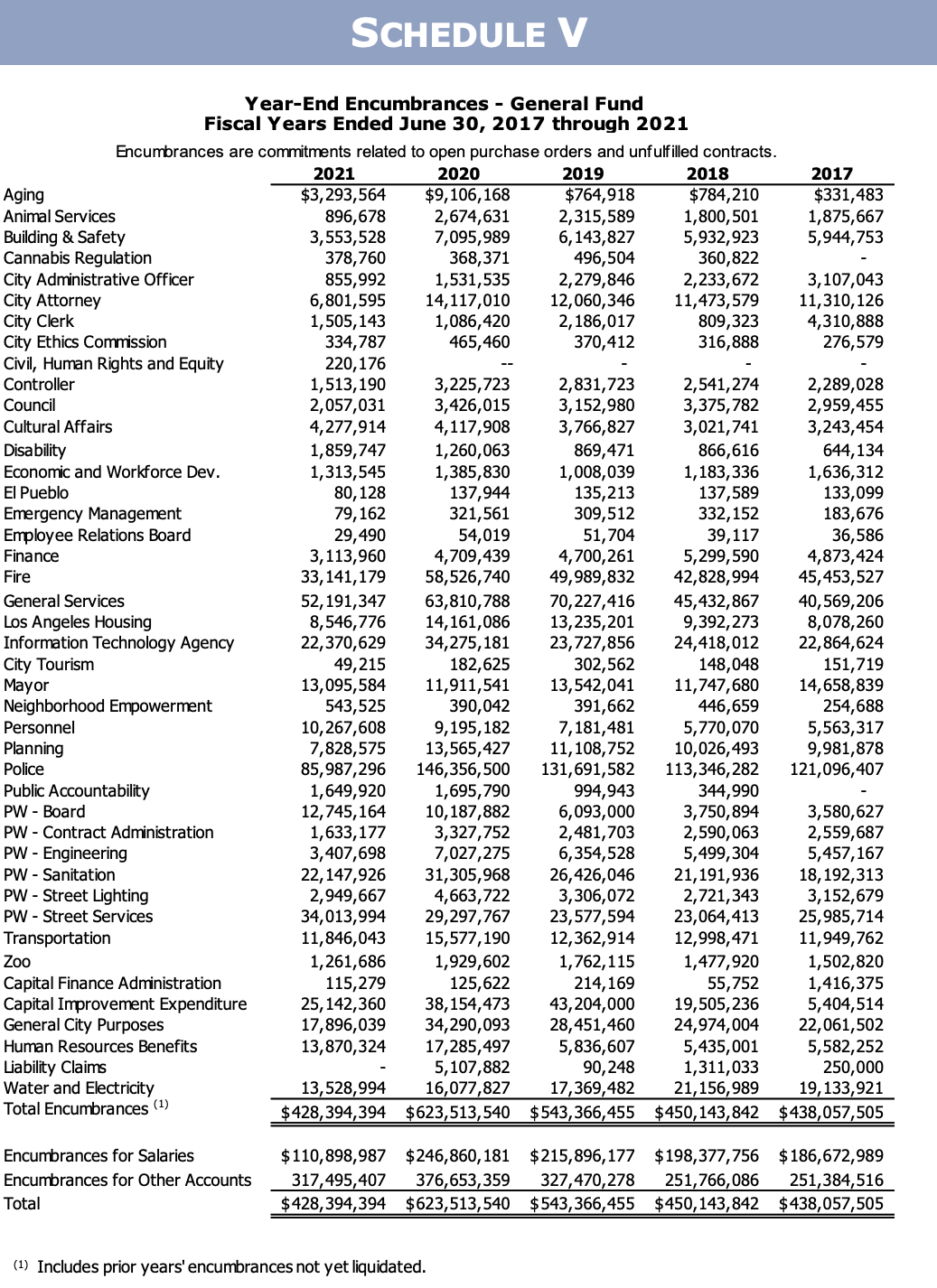

Encumbered funds for salaries are earmarked for the last pay period of the fiscal year and unspent funds are immediately released after payroll is made. Funds encumbered for expense accounts are continued across fiscal years to ensure that cash is available to cover the expenditure when it is made. Schedule V provides a listing of General Fund encumbrances by department.

The General Fund Encumbrance Policy provides that encumbered funds that remain unspent for a period longer than one Fiscal Year shall be disencumbered every fiscal year, with the exception of capital project funds. Prior-year encumbrances are automatically disencumbered unless exempted by Mayor and Council approval. As part of the 2020-21 Year-End Financial Status Report, a total of $53.0 million was exempted from being disencumbered, a decrease of $4.1 million from last year’s exemptions. As noted in past years, this is an issue which deserves more attention.

Unencumbered General funds revert to the Reserve Fund at year end. As such, exemptions to the automatic disencumbrance policy reduce reversions, thereby reducing the cash available in the Reserve Fund to pay for emergencies and contingencies. Section II below discusses the status of the Reserve Fund in more detail.

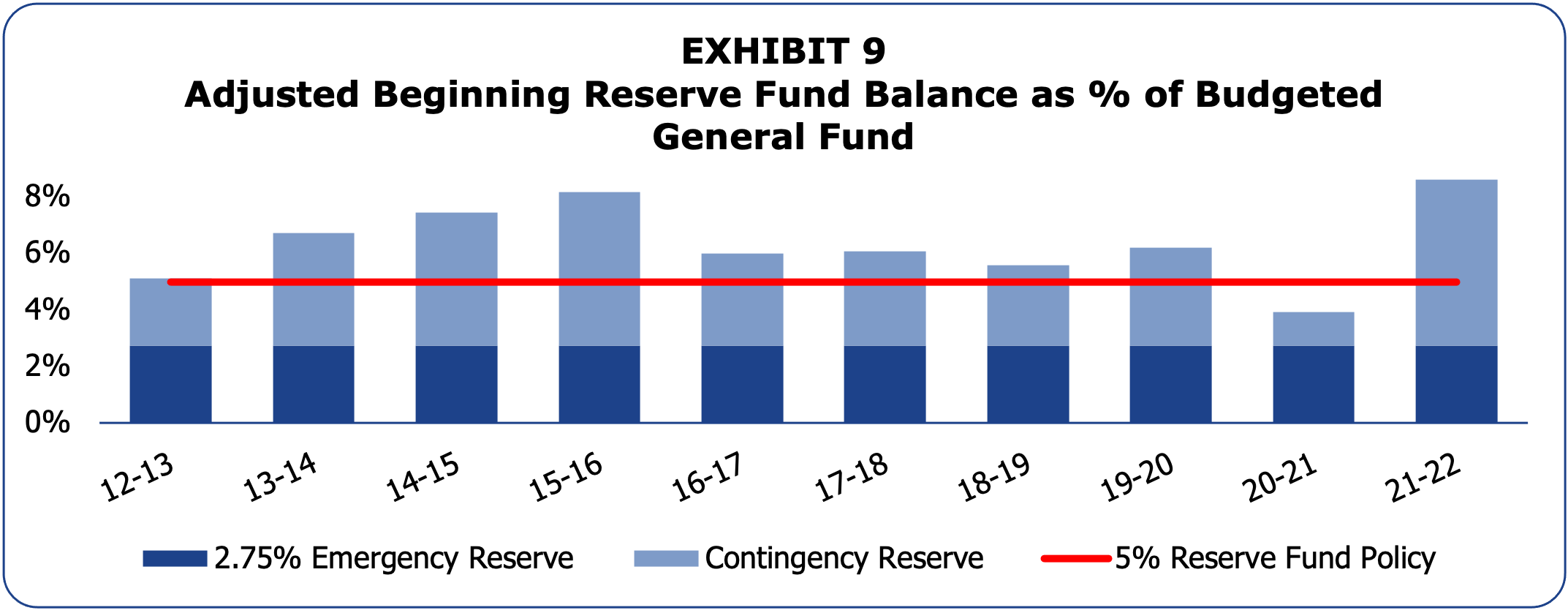

The Reserve Fund is established to ensure that funds are available for unanticipated expenditures and revenue shortfalls in the General Fund, and is broken into an Emergency Account and a Contingency Account.

The Emergency Reserve Account is fixed at 2.75 percent of the adopted General Fund receipts. A finding of urgent economic necessity is required to use these funds. The Contingency Reserve Account includes all monies in the Reserve Fund over and above the amount required to be allocated to the Emergency Account. Contingency Reserve Account funds can be a source of additional funding to cover unanticipated expenses or revenue shortfalls.

The City’s Reserve Fund Policy (CF 98-0459) sets a Reserve Fund cash balance goal of at least 5.0 percent of budgeted General Fund receipts. Exhibit 9 displays the past ten years of beginning Emergency and Contingency Reserve Fund balances compared to this policy target.

The Reserve Fund is a major indicator of the City’s fiscal health, and is vital to cash flow, bond ratings, and the ability to manage financial challenges as we did in 2019-20, when almost $200 million from the Reserve Fund to balance the General Fund revenue shortfall.

Failure to keep the City’s Reserve Fund at an appropriate level not only exposes the City to significant risk in the event of an emergency, but can also have negative financial impacts due to increased cost of borrowing.

Reserve Fund Status

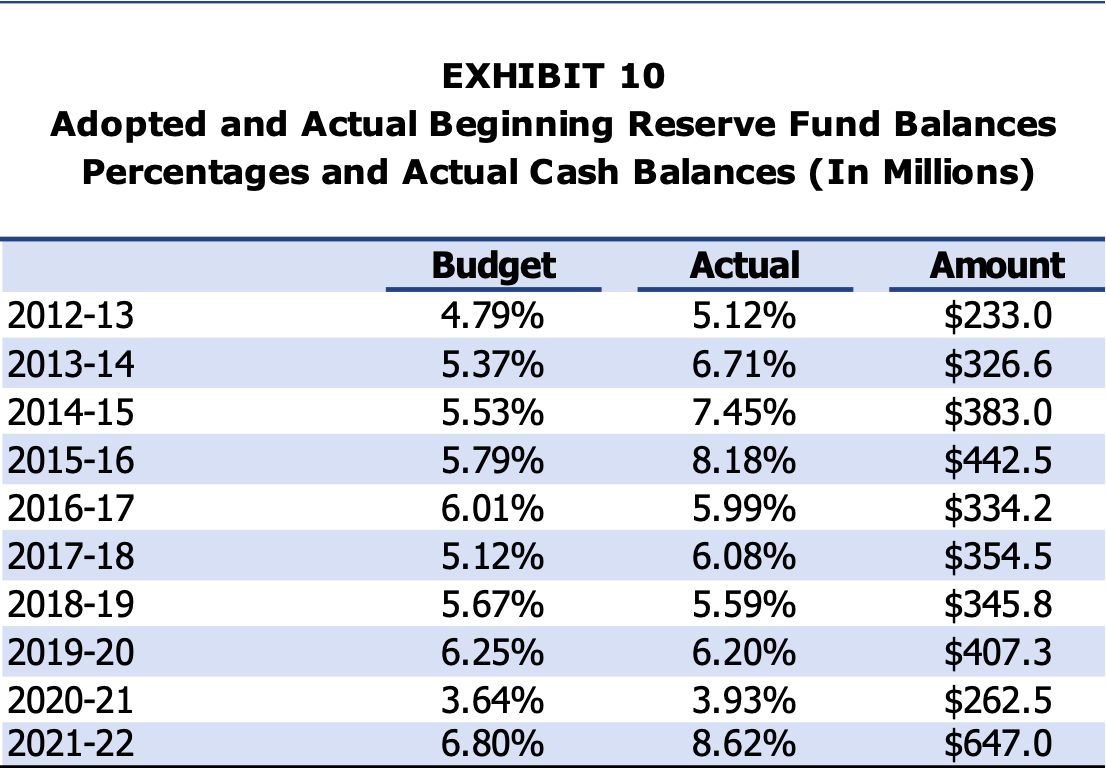

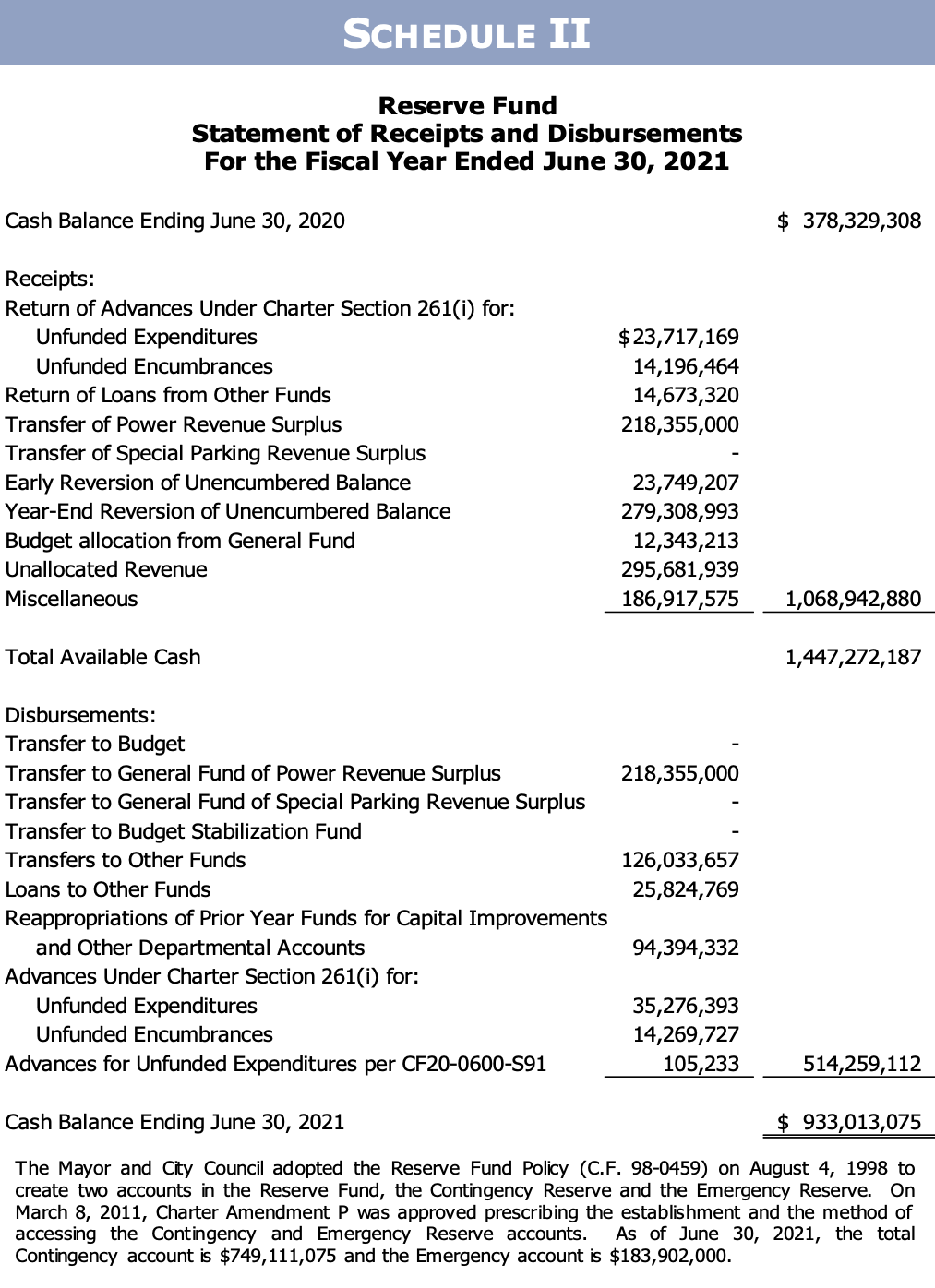

After the 2020-21 accounting close, budgetary appropriations, return of advances, and reappropriations, the Fiscal Year-start adjusted Reserve Fund balance was $647.0 million or 8.62 percent of General Fund receipts anticipated in the 2021-22 Budget, $271.9 million above the 5.0 percent Reserve Fund Policy goal.

Exhibit 10 shows Adopted and Actual Beginning Reserve Fund Balances for last ten years.

The Beginning Reserve Fund balance for 2021-22 is at the highest level for the last ten years, after reaching the lowest in 2020-21, and is $137.2 million more than the assumed in the Fiscal Year 2021-22 Adopted Budget.

Adjustments to the Reserve Fund Cash Balance

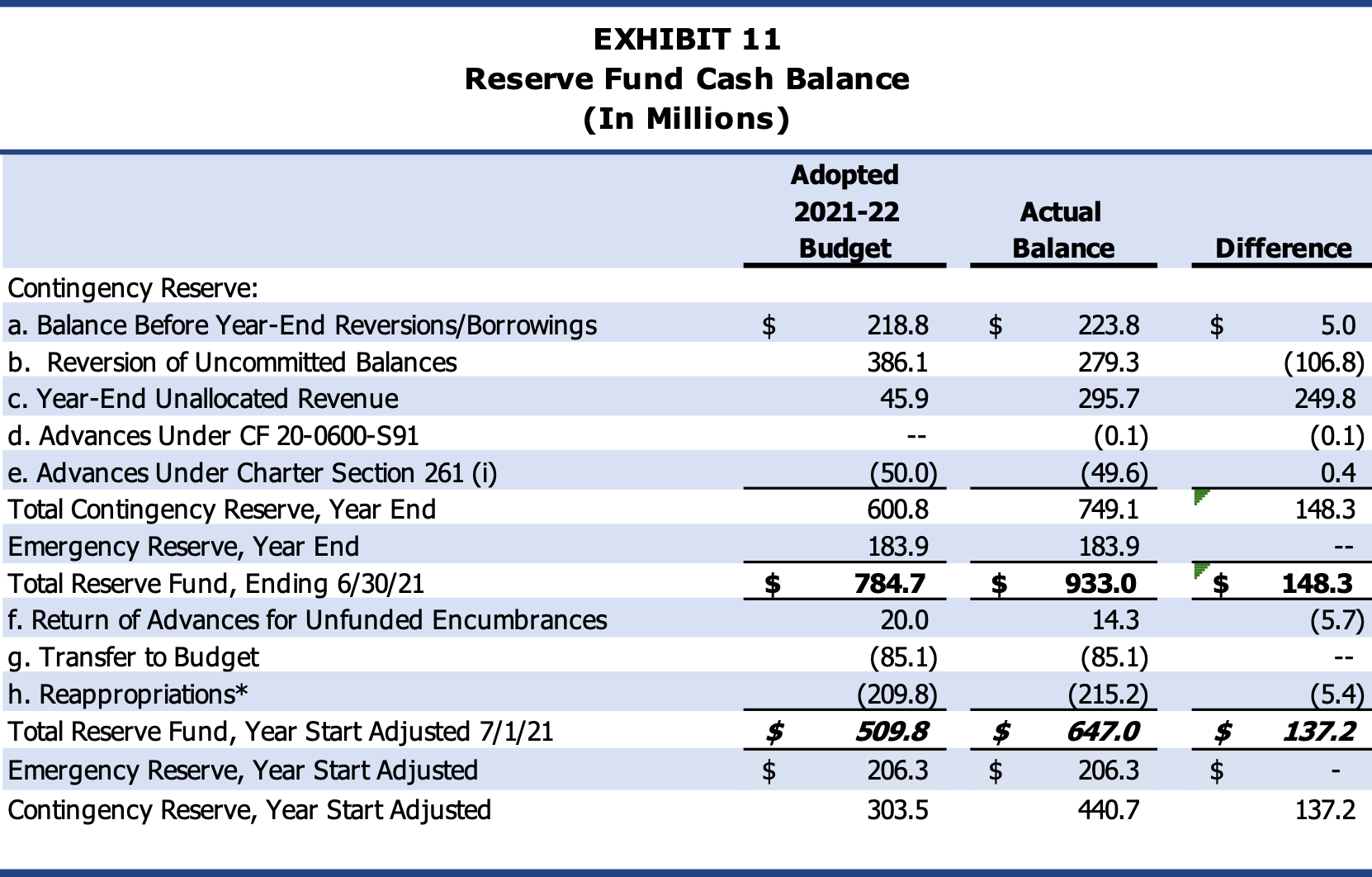

At the end of each Fiscal Year and the beginning of the next, a number of transactions are required to accurately reflect the status of the Reserve Fund through the closing of the City’s books. Exhibit 11 details the year-end and year-start adjustments to the Reserve Fund Cash Balance, comparing Budget versus actual.

* Reappropriations and Transfer to Budget are actually completed after July 1.

Following are descriptions of the line item changes to the Reserve Fund listed in Exhibit 11:

Reserve Fund Cash Balance (June 30, 2021)

As of June 30, 2021, after closing the City’s General Ledger, the recorded Reserve Fund balance was $647.0 million. This was $137.2 million more than the amount anticipated in the 2021-22 Budget. The Reserve Fund cash balance is adjusted by the following factors to arrive at the year-end balance:

- Balance Before Year-End Reversions/Borrowings

The amount of cash available in the Contingency Reserve prior to adjustments for year-end reversions, unallocated revenues, and borrowings. It does not include cash in the Emergency Reserve. For 2020-21, this amount was higher than anticipated in the budget due to higher than anticipated return of advances and early reversion made after the adoption of the budget.

- Reversion of Uncommitted Balances

Uncommitted General Fund appropriations are reverted to the Reserve Fund at fiscal year-end. Appropriations (spending authority) granted to City departments by the Mayor and Council are committed throughout the year in the form of encumbrances and expenditures. Remaining or uncommitted balances are reverted to the Reserve Fund to the extent that there is available cash in the General Fund.

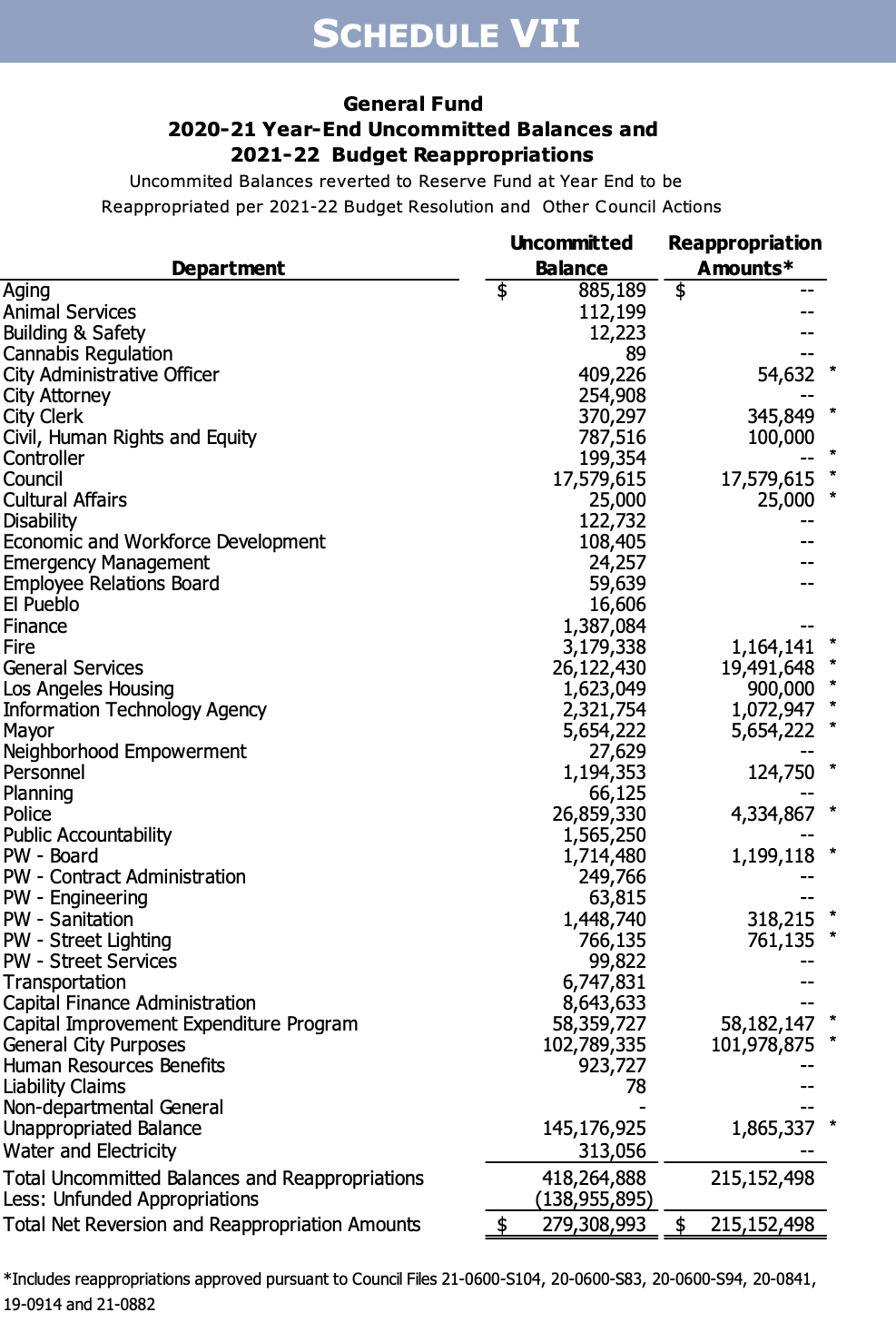

In 2020-21, the budget estimated $386.1 million in reversions. The uncommitted balance at year end was $418.3 million. Excluding unfunded appropriations, a total of $279.3 million reverted to the Reserve Fund. For a detailed breakdown of uncommitted balances by department, please see Schedule VII.

- Year-End Unallocated Revenue

Unallocated revenue occurs when revenues exceed the total budget appropriation. At Fiscal Year-end, excess receipts of $295.7 million reverted to the Reserve Fund as unallocated revenue. The 2021-22 Adopted Budget anticipated $45.9 million in unallocated revenue. Actual receipts were $249.8 million more than the budgeted unallocated revenue.

- Advances Under CF 20-0600-S91

Council File 20-0600-S91 authorized the Controller to borrow from the Reserve Fund at year-end to balance departmental budgets where needed in order to facilitate the closing of the City’s General Ledger. The Controller is authorized to increase appropriations within established limits without getting itemized Mayor and Council approval, a process that would delay the closing of the City’s General Ledger. Advances were made to Fire and Personnel Departments in the amount of $83,320 and $21,913 respectively.

- Advances Under Charter Section 261(i) for Unfunded Encumbrances and Expenditures

Under Charter Section 261(i), the Controller transfers funds from the Reserve Fund as a loan to any fund that becomes depleted due to tardy receipt of revenue. The 2021-22 Budget estimated $50.0 million in year-end advances. Actual advances were $49.6 million, consisting of $35.3 million in unfunded expenditures and $14.3 million in unfunded encumbrances. See Schedule VIII for a breakdown by department.

Unfunded expenditures generally occur when transactions take place prior to receipt of funding (e.g. grants on reimbursement basis) and/or due to billing delays. When the funding source reimburses the costs, departments are able to repay the advances. If funding is not available, departments may request Mayor and Council approval to write-off the advances. Unfunded encumbered amounts represent a technical adjustment at year-end and are reversed at the start of the new Fiscal Year as documented in item (f), below.

Reserve Fund Cash Balance (2021-22 Year-Start)

The year-end Reserve Fund cash balance is not the same as the year-start cash balance for the next year. The following technical adjustments are made after the close of the prior Fiscal Year, but are accounted for in determining the year-start cash balance:

- Return of Advances for Unfunded Encumbrances

Advances for unfunded encumbrances are reversed at the start of the following fiscal year, as discussed in item (e), above.

- Transfer to Budget

The 2021-22 Budget includes $85,090,146 transfer from Reserve Fund to Budget, which is made during the Fiscal Year by the Controller depending on the cash condition.

- Reappropriations

The 2021-22 Budget and other Council actions (C.F. 21-0600-S104, 20-0600-S83, 20-0600-S94, 20-0841, 19-0914, and 21-0882) provided that certain uncommitted balances earmarked for specific programs would be reappropriated in the subsequent year if not expended by the year-end. See Schedule VII for reappropriations by department. Actual reappropriations of $215.2 million were $5.4 million above the estimated $209.8 million Budget.

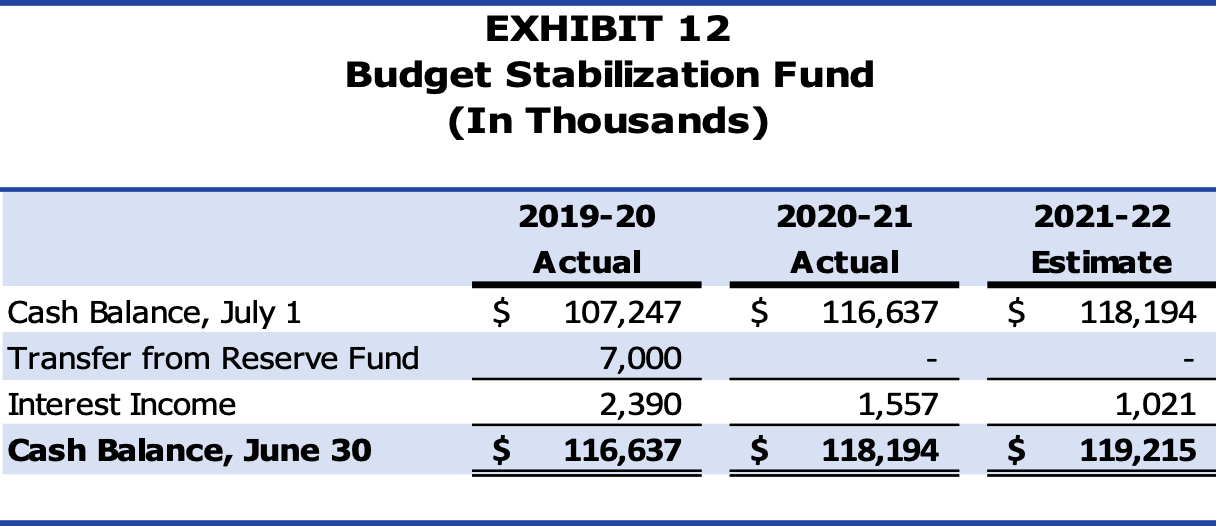

The Budget Stabilization Fund (BSF) was added to the City’s Charter in 2011. The purpose of this fund is to set aside revenues during periods of robust economic growth or when revenue projections are exceeded to help smooth out years when revenue is stagnant or is in decline. The BSF does not have a minimum balance that must be maintained.

The June 30 BSF cash balance was $118.2 million. Exhibit 12 displays the adopted and prior year cash balance and adjustments of the BSF. The Budget does not include a deposit into the Fund after 2019-20.

The current BSF Policy (approved January 21, 2020) states that a budget appropriation shall be included as part of the Budget for the following fiscal year when the anticipated growth in combined receipts from seven City “economically sensitive” revenue categories (Property Tax, Utility Users Tax, Business Tax, Sales Tax, Documentary Transfer Tax, Transient Occupancy Tax, and Parking Users Tax) exceeds the growth threshold. For each five-tenths of one percent that the anticipated growth exceeds the growth threshold, the amount of the required appropriation to the BSF shall be equal to five percent of the value of the anticipated excess growth. The maximum appropriation shall be equivalent to 25 percent of the value of the growth above the growth threshold. For Fiscal Year 2021-22, the growth rate used to determine BSF contributions was recalculated to be 4.1 percent, based on the 20-year historical average of these tax revenues.

The required deposit to the BSF may be forgone completely in the case that the City Council and Mayor declare a fiscal emergency or suspend the BSF funding policy based on findings that it is in the best interest of the City to suspend the policy. Mid-year deposits to the BSF or deposits above the required amount may be authorized by the City Council, subject to the approval of the Mayor, at any time during the year from various General Fund sources. Consideration should be given to depositing unanticipated and unbudgeted receipts that are not otherwise required to balance the current year budget.

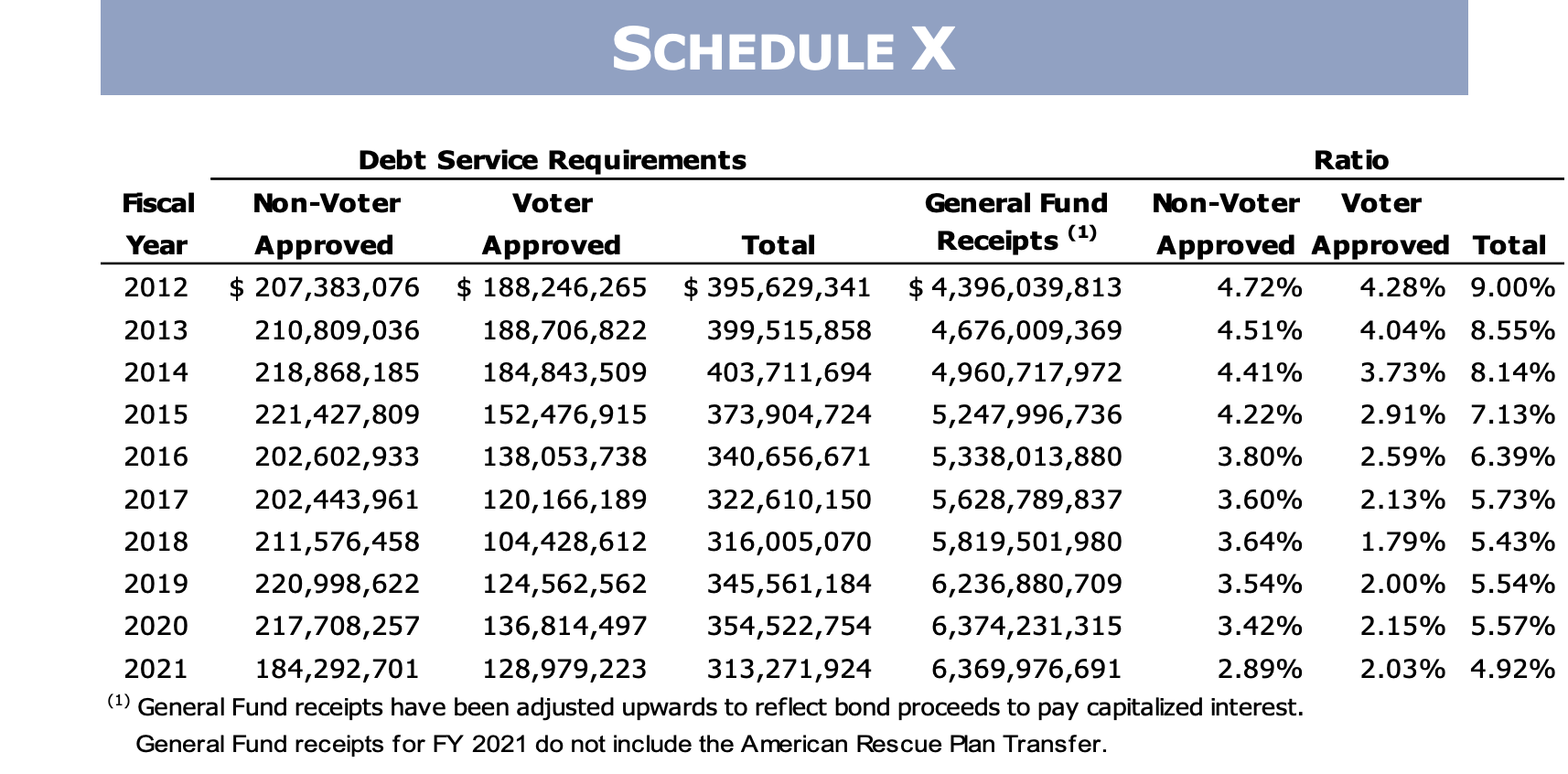

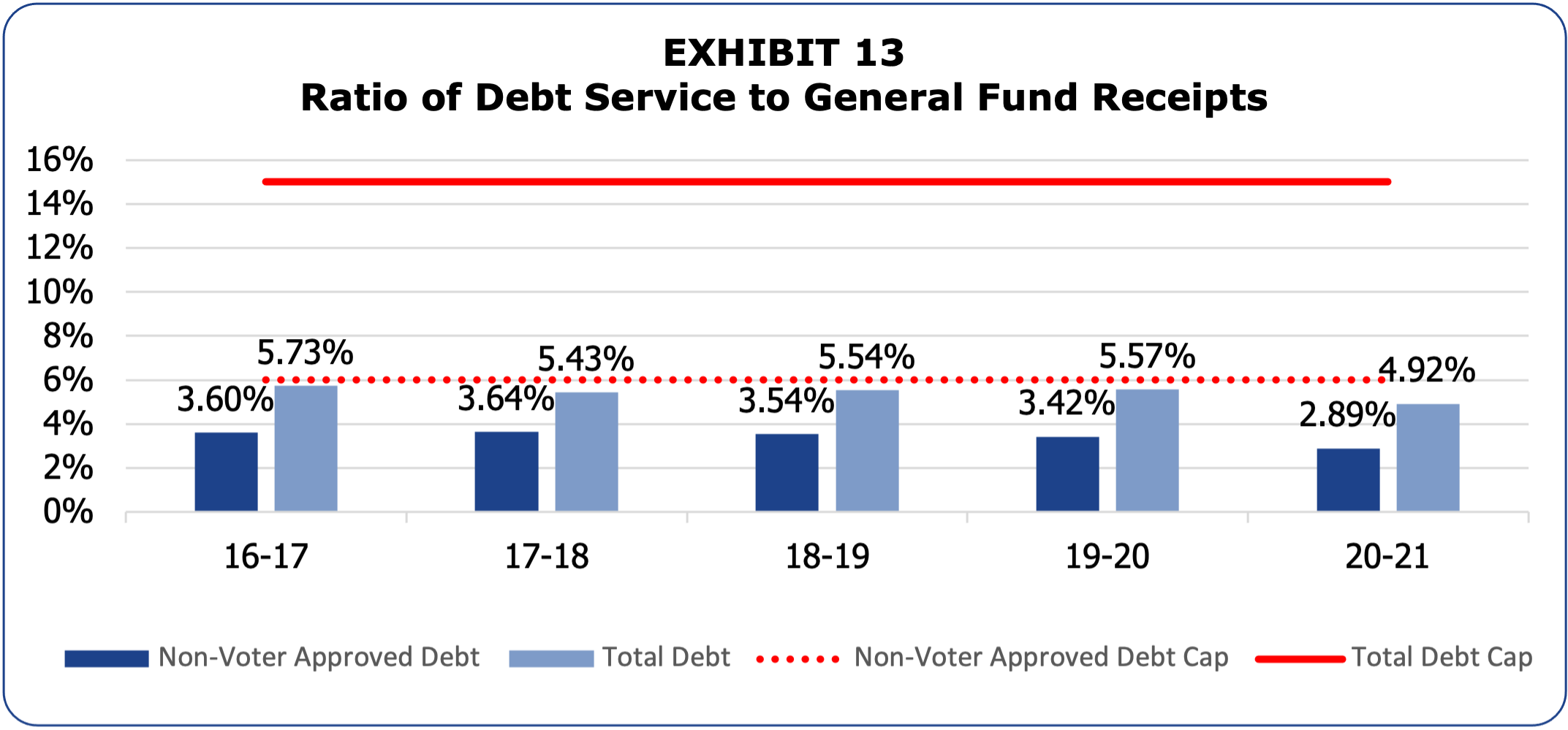

The City’s Debt Management Policy creates guidelines for the structure and management of the City’s debt obligations. These guidelines include target and ceiling levels for certain debt ratios to be used for planning purposes. The two most significant ratios are a non-voter-approved debt service cap as a percent of General Fund revenues of 6 percent and a total debt service cap as a percent of General Fund revenues of 15 percent.

Exhibit 13 illustrates the City’s compliance with these debt management policies for the past five years.

The actual ratio of Debt Service to General Fund Receipts (excluding the ARPA transfer of $639.5 million) was 4.92 percent in 2020-21, comprised of 2.89 percent for non-voter approved debt and 2.03 percent for voter approved debt. The ratio decreased due to defeasance and advance refunding of MICLA Revenue Bonds Series 2014 and 2019. Schedule IX shows the details of Outstanding General Obligation Bonded Debt.

Exhibit 13 above shows very clearly the responsibility the City has exhibited when it comes to debt management. Good administration of debt service obligations has put the City in a position to consider major projects, as well as making strategic financing agreements available when these present financial advantages.

This significant amount of debt capacity also indicates an opportunity to invest in large-scale long-term infrastructure projects, including both facility repair and replacement as well as new projects designed to stimulate economic development. Such an investment would also provide an opportunity to focus on regional equity, focusing investment in areas of the City which have often been left behind in prior initiatives. More generally, a significantly expanded capital program would serve as a fiscal stimulus for the entire region, adding jobs to a struggling economy and providing the infrastructure for future opportunity.

Over the coming years, the City will emerge from the public health and economic crises we’ve been experiencing. This period will feature political transitions as well as economic transitions. The City’s immediate fiscal position is strong, but the many critical priorities and limited ongoing funding will demand difficult choices and careful financial management by the City’s leaders. To this end, we make the following recommendations:

Recommended actions

-

Strengthen the City’s revenues and control ongoing costs.

While some revenues have remained strong through the current crisis, others have decreased significantly. It is critical to the City’s recovery that revenue generation and collection be restored. At the same time, we must limit growth in the City’s ongoing costs so that we do not commit to unsustainable levels of future spending.

-

Build on successful new programs and consider ending those that are not delivering results.

The Fiscal Year 2021-22 Budget provides significant funding to begin pilot projects and new programs. The City should analyze these efforts critically and commit to ongoing funding only for those programs which demonstrate success.

-

Maintain the City’s strong Reserve Fund.

After a decade of building up the Reserve Fund, the City used almost $200 million to offset a General Fund shortfall at the end of Fiscal Year 2019-20. Now, with the largest Reserve Fund the City has ever had, there will naturally be a temptation to treat it as a source of funds for new programs. However, these reserves should be guarded and only used to fund the most critically important, one-time programs, or this important tool will not be available the next time it is needed.

-

Utilize the City’s capital program and debt capacity to meet critical needs and drive equity.

As part of the effort to reduce expenditures during the first half of Fiscal Year 2020-21, funding was cut from a large number of capital projects. The next budget year will likely see a rebuilding of the City’s capital program, providing a perfect opportunity to leverage capital needs and build equity in the City’s under-resourced and disadvantaged neighborhoods and people.

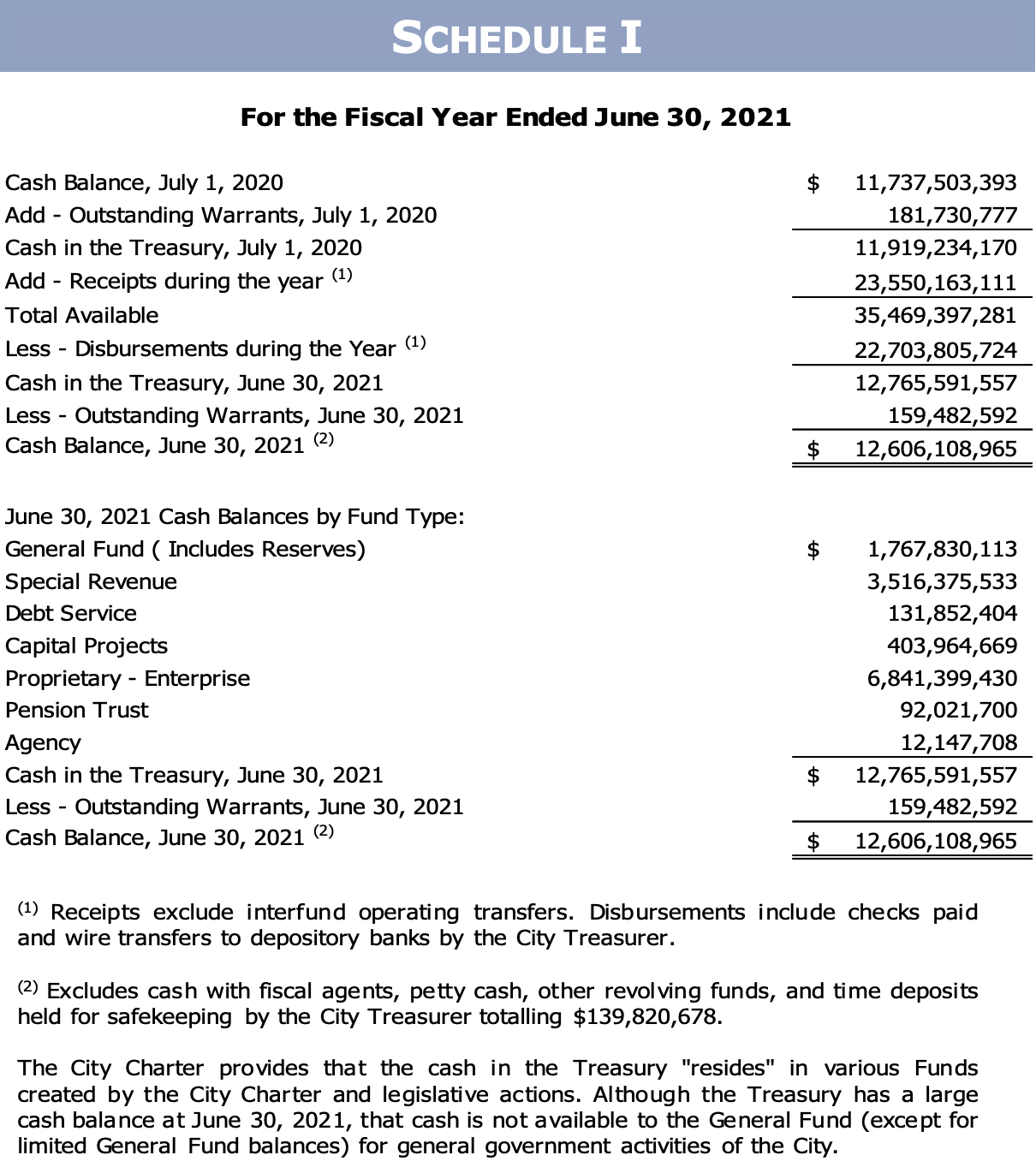

Schedule I: Cash Condition Statement of Receipts and Disbursements

Schedule II: Reserve Fund Statement of Receipts and Disbursements

Schedule III: Statement of Receipts – Budget and Actual (Cash Basis) – All Annually budgeted Funds

Schedule IV: Statement of Budget Appropriations, Expenditures and Encumbrances Budget and Actual (Cash-Basis) – All Annually Budgeted Funds

Schedule V: Year-end Encumbrances – General Fund

Schedule VI: General Fund Unencumbered Balances Reverted to the Reserve Fund

Schedule VII: General Fund Year-End Uncommitted Balances and Adopted Budget Reappropriations

Schedule VIII: Year-End Advances from the Reserve Fund for Unfunded Expenditures and Encumbrances

Schedule IX: Statement of General Obligation Bonded Debt

Schedule X: Ratio of Debt Service Requirement to General Fund Receipts Last Ten Fiscal Years